Wholesale & Distribution Insurance

"From Warehouse to Doorstep — Fully Covered."

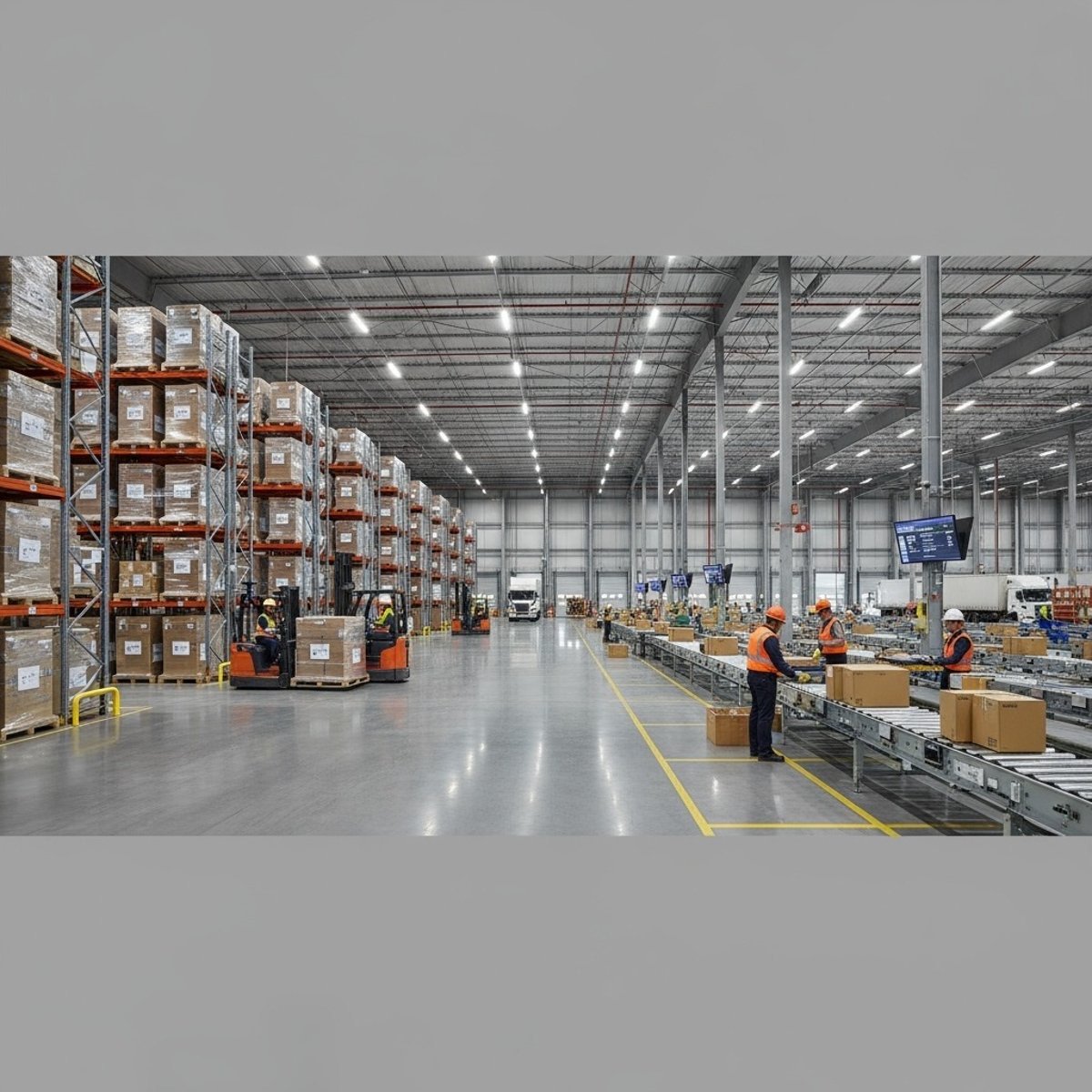

Wholesale & Distribution Insurance

Protecting inventory, shipments, and supply chain operations

Wholesalers and distributors face constant exposure to inventory loss, transportation risks, contractual obligations, and liability claims. Businesses that store, move, and deliver goods must manage risks related to warehouses, cargo, vendors, and customers. Damage to products, delays in delivery, or accidents during transport can quickly lead to financial loss or contract disputes.

Properly structured insurance helps protect inventory, facilities, and the flow of business operations.

Key Risks in Wholesale & Distribution Operations

Wholesalers and distributors face exposure related to:

Inventory damage or theft

Warehouse property loss

Cargo loss during transit

Product liability claims

Vendor and supplier disputes

Equipment or forklift accidents

Business interruption after a loss

Losses can occur at any point in the supply chain.

Core Coverages for Wholesale & Distribution Businesses

Wholesale and distribution insurance programs typically include:

General Liability — Protects against bodily injury and property damage claims involving customers, vendors, or third parties.

Commercial Property — Covers warehouses, storage areas, equipment, and inventory against covered physical loss.

Product Liability — Protects against claims involving products sold, distributed, or supplied.

Inland Marine / Cargo Coverage — Protects goods while in transit or stored off-site.

Warehouse Legal Liability (when applicable)Covers damage to goods stored on behalf of others.

Workers Compensation — Provides coverage for employee injuries as required by law.

Commercial Auto — Covers vehicles used for delivery, transport, or business use.

Umbrella / Excess Liability — Provides additional limits for severe claims.

What’s Commonly Overlooked

Wholesale insurance programs are often weakened by:

Underinsured inventory values

Missing cargo or transit coverage

No warehouse liability protection

Inadequate product liability limits

Gaps between property and inland marine

Failure to update coverage as inventory grows

These issues often appear only after a major loss.

Real-World Claim Examples

Inventory is damaged in a warehouse fire

A shipment is lost during transit

A forklift accident injures a visitor

A product causes injury to a customer

A storm damages stored goods

Even one loss can interrupt the entire supply chain.

Why Proper Placement Matters

Wholesale and distribution coverage varies based on:

Type of products handled

Inventory value and storage methods

Shipping and delivery exposure

Warehouse size and location

Contract requirements

Use of third-party carriers

Improper placement can lead to uncovered losses or contract disputes.

Our Approach

At Cory Washington & Co., we structure wholesale and distribution insurance programs based on how your products move, where they are stored, and the contracts you operate under. We coordinate property, cargo, liability, and warehouse coverage to ensure your protection follows the entire supply chain.

When your business depends on movement, your insurance must move with it.

Available in all 50 states. See how requirements differ in California, Texas, Florida, New York, or choose your state.